Public Insight’s December 2025 Jobs Report summarizes market insights from the millions of job postings, resumé updates and employer ratings/reviews available in our TalentView talent market intelligence platform.

Summary Dashboard – December 2025 Jobs Report

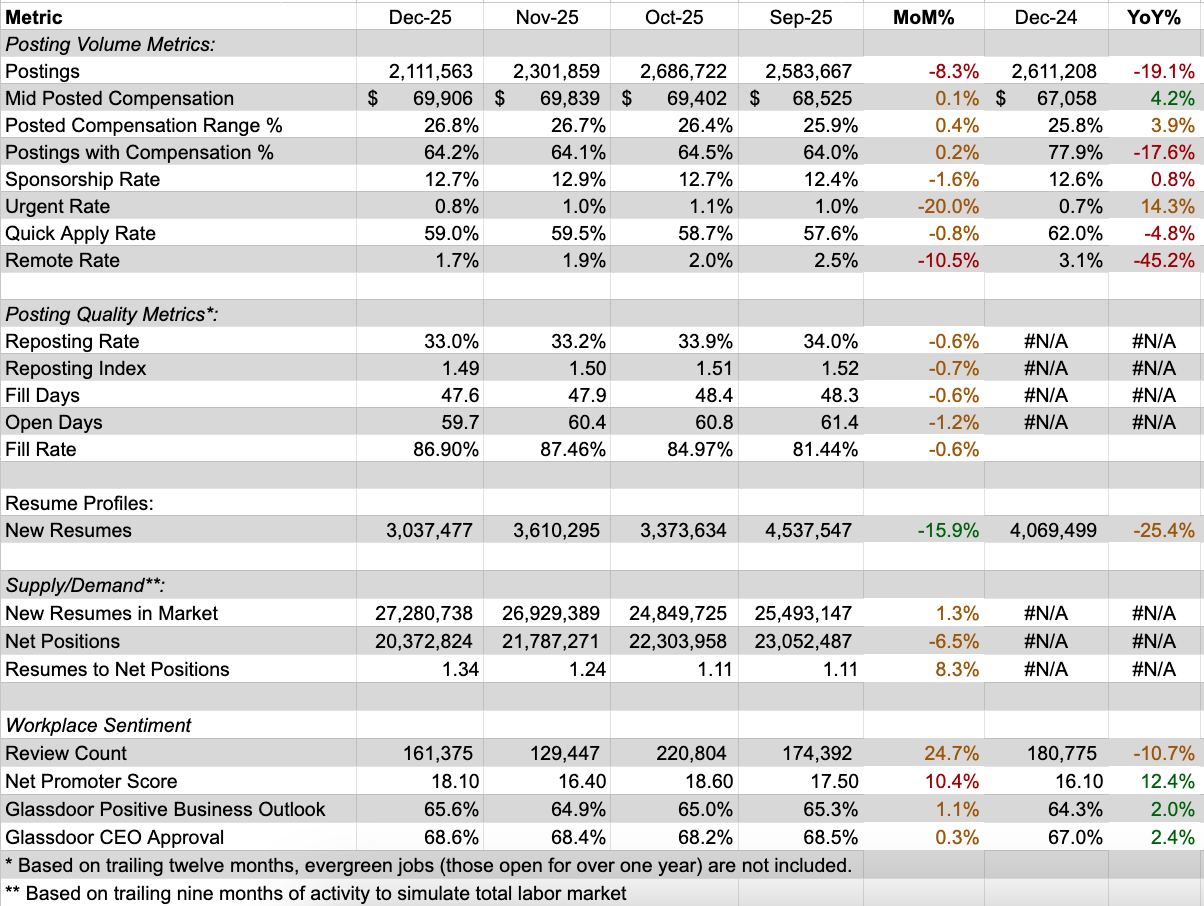

Comparisons of Key Metrics from December to November, October and September 2025 and to December 2024

Postings

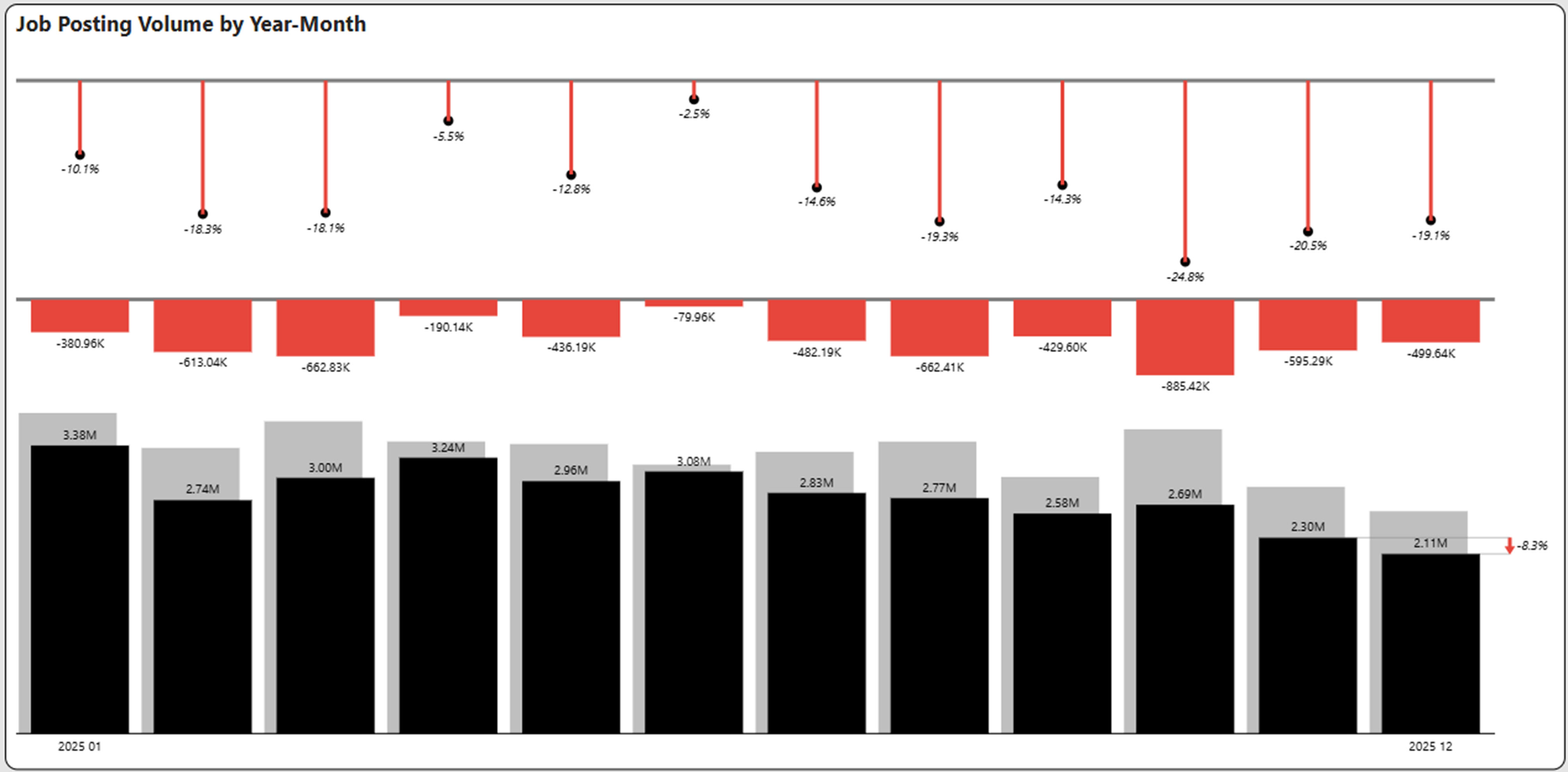

Posting Volume: A Lost Year

December job postings declined 19.1% from the same period last year to 2.11 million. December posting volume was sequentially down 8.3% from November and represents the lowest monthly posting volume of 2025. As shown below, postings have declined from 2.5% to 24.8% each month in 2025 from the comparative period in 2024.

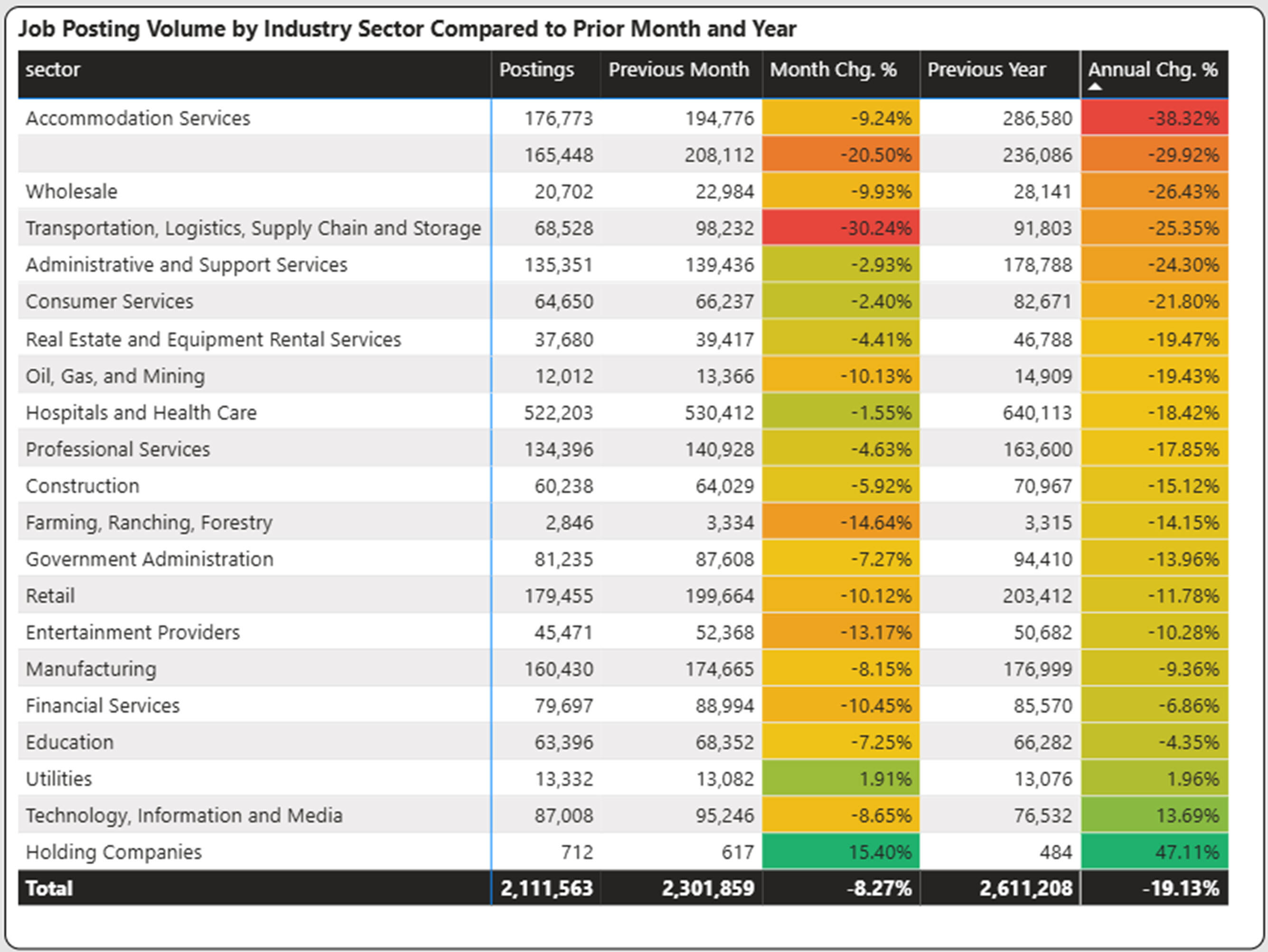

Industry Posting Analysis

Every sector in December 2025 declined from 2024 except for Utilities, Technology, Information, and Media and Holding Companies. Only Utilities and Holding Companies had an increase in postings from November to December.

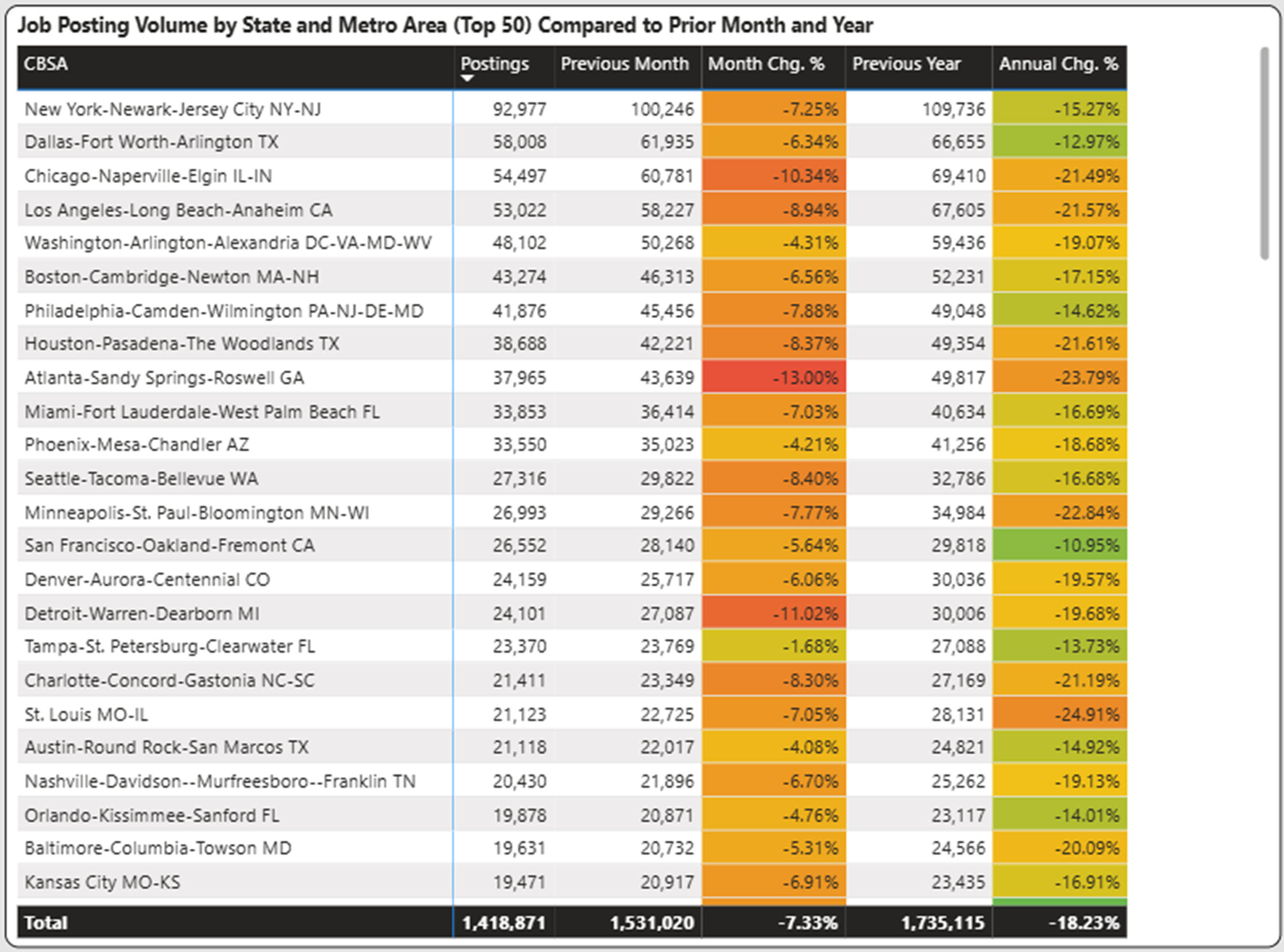

Regional Analysis

All large cities (Top 50) experienced sizeable year-over-year declines as shown below. While no regions have been exempted from the posting declines, mid-size cities have declined less on a year-over-year basis. As an example, Madison, WI, and Salt Lake City (not shown) have experienced more resilience with year-over-year declines of less than 10%.

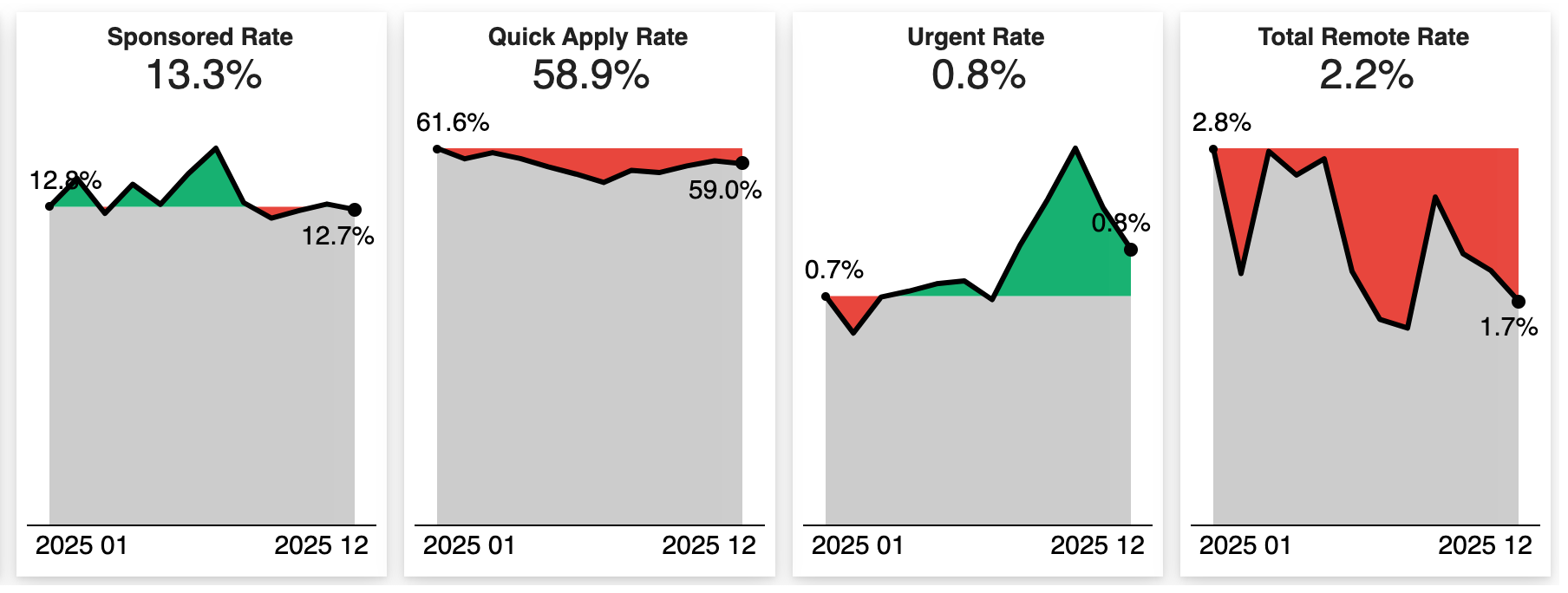

Indicator Rates – Sponsored, Quick Apply, Urgent and Remote

Sponsored rate is the percentage of job advertisements that have had a paid sponsorship at some point over the time period. This is a measure of job boards’ activity. Sponsored rates ranged between 12.4% and 15.2% with the December rate of 12.7% decreasing 1.7% from November.

Quick apply rate is an indicator of whether a job posting has the quick apply feature. It also has shown some sustained improvement in December and stands 3.5% above the lowest point at 56%, but well below the peak of 61.6% at the start of the year.

Urgent rate is the percentage of jobs that have been indicated as urgent at some point over the time period. Urgent rate hit its highest mark in October at 1.1%.

Total remote rate is the rate of jobs that have been advertised at some level of remote. December’s rate of 1.7% is .2% lower than the November rate of 1.9%

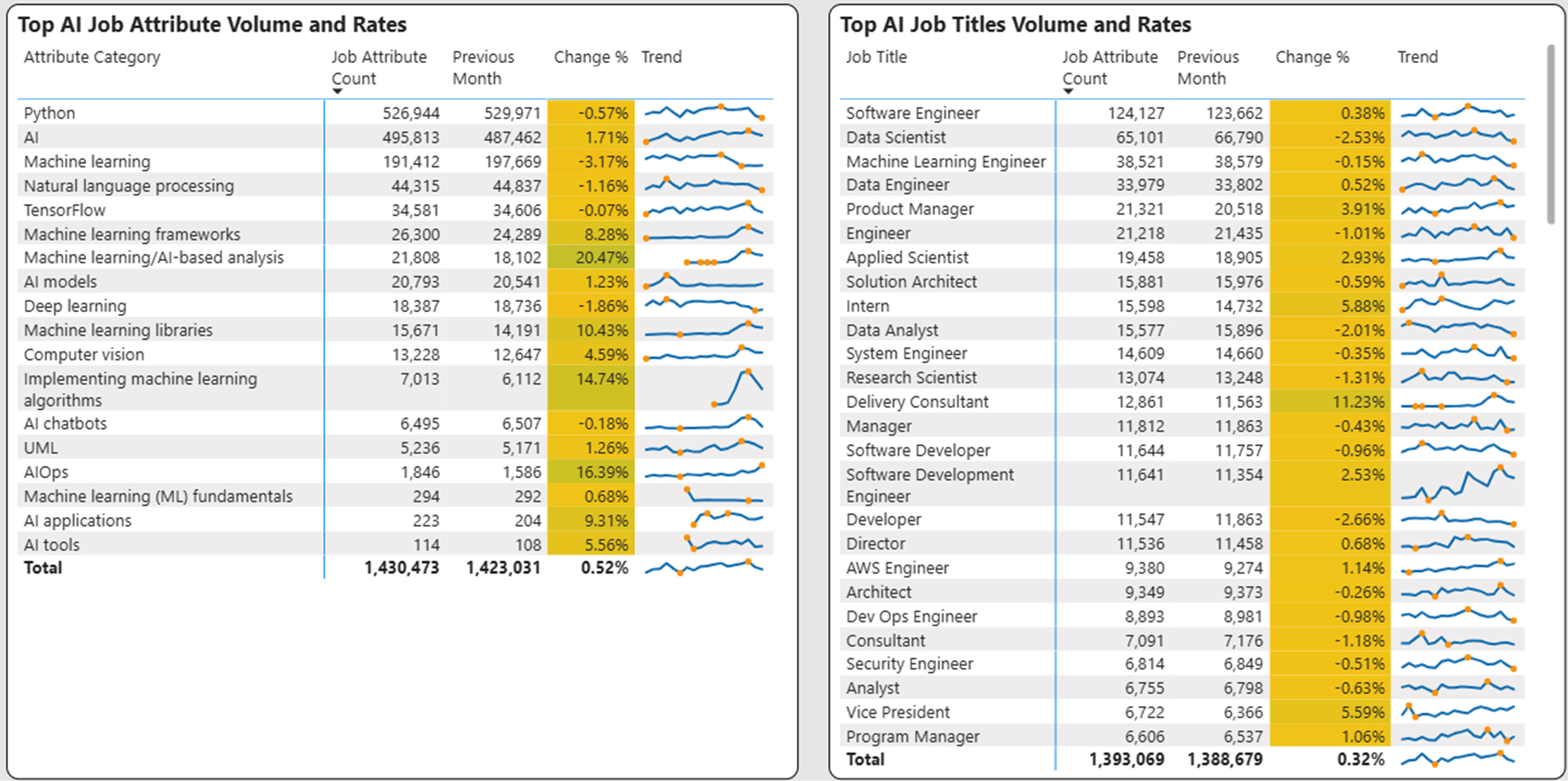

Artificial Intelligence (AI) Skills Growth

Job attributes are categories of skills, benefits or credentials that are included in a job posting. We have flagged AI related categories and plotted the trailing 17-month (earliest data available) growth as shown below. The decline in December AI attributes of 10% is favorable compared to the decline in overall job posting growth of 19.1%.

The top AI skills are shown below along with the corresponding job titles. Python has remained the top mentioned attribute while machine learning related attributes continue to show the most growth. These attributes are infused across multiple technology job titles but are also increasingly showing up in non-technical job titles such as product manager and delivery consultant.

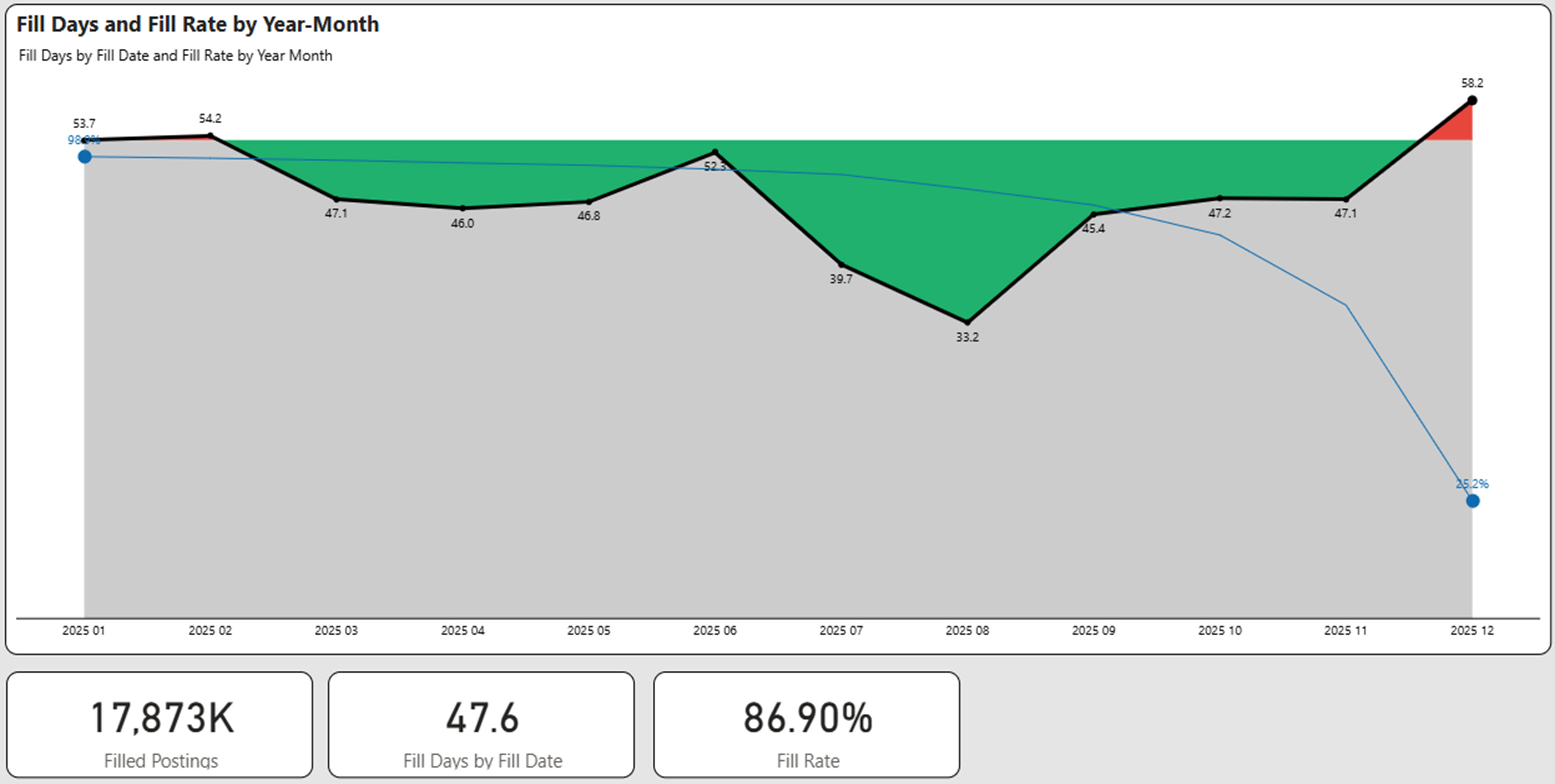

Fill Days are Flat – Still Indicating Success at Filling Jobs

For fill days we use ad expiration and ad removal to determine a presumptive hire. When measured over a prolonged period of time and over millions of postings, this provides a strong view of the overall market. The trailing 12 months is used as a time period for our analysis.

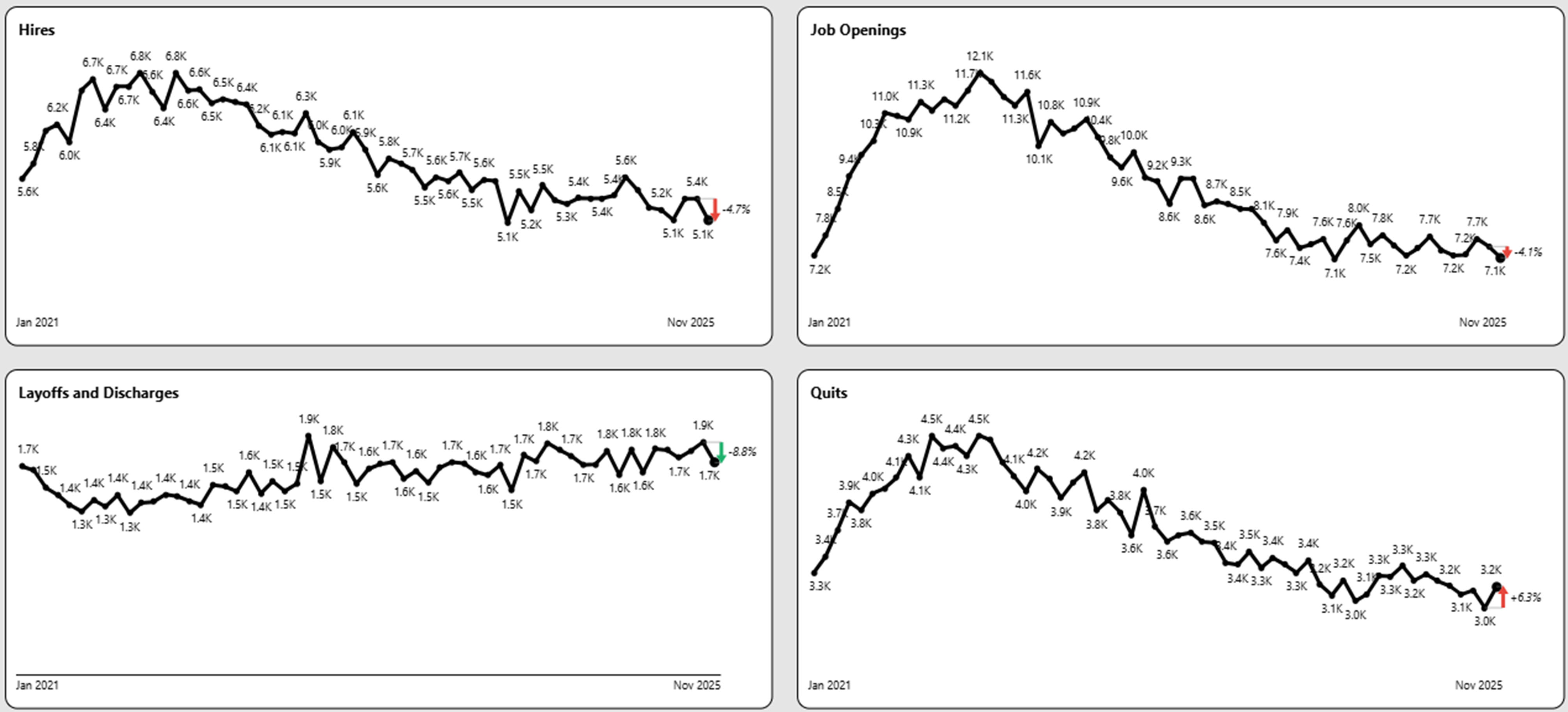

In the graph below, we show the fill days by month along with the percentage of ads (blue line) that have been filled. Obviously, the newer ads have a lower fill rate.

Fill days and fill rates were pretty much flat in December. The average over the time period for fill days decreased slightly in December from 47.9 days to 47.6 days and fill rates also decreased slightly from 87.5% to 86.9%, still indicating good success in filling jobs.

Open Days and Open Postings Shows Little Change in December

We track every job posting uniquely and ascertain its fill status on a weekly basis. Open days is the age of postings that are still determined to be open. Generally, we have found that 12 months to be a suitable time period to evaluate the age of open days. Older postings may distort the open days as they may represent “evergreen” postings. For this reason we eliminate implied evergreen ads that are older than one year from our analysis.

The graph below shows the aging of open postings for the past 12 months. Open days was flat in December compared to November at 59.7 days. The percentage of open jobs increased slightly from November at 13.1%, but well below the peak of 15%. The number of open jobs remains approximately 2.7 million. Clearly between fill days and open days, the job market is tightening.

Compensation

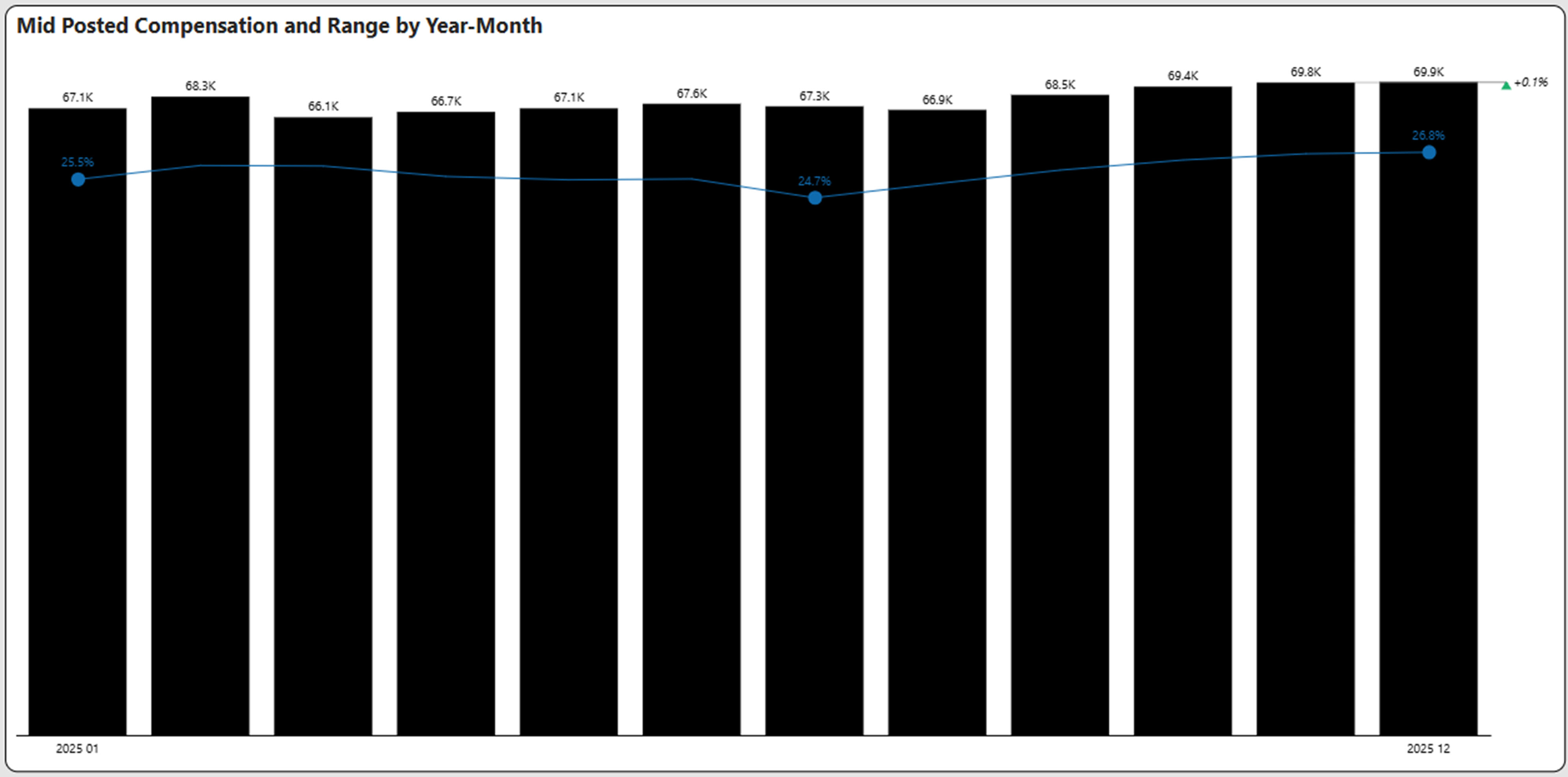

Comp is Flat at $70k

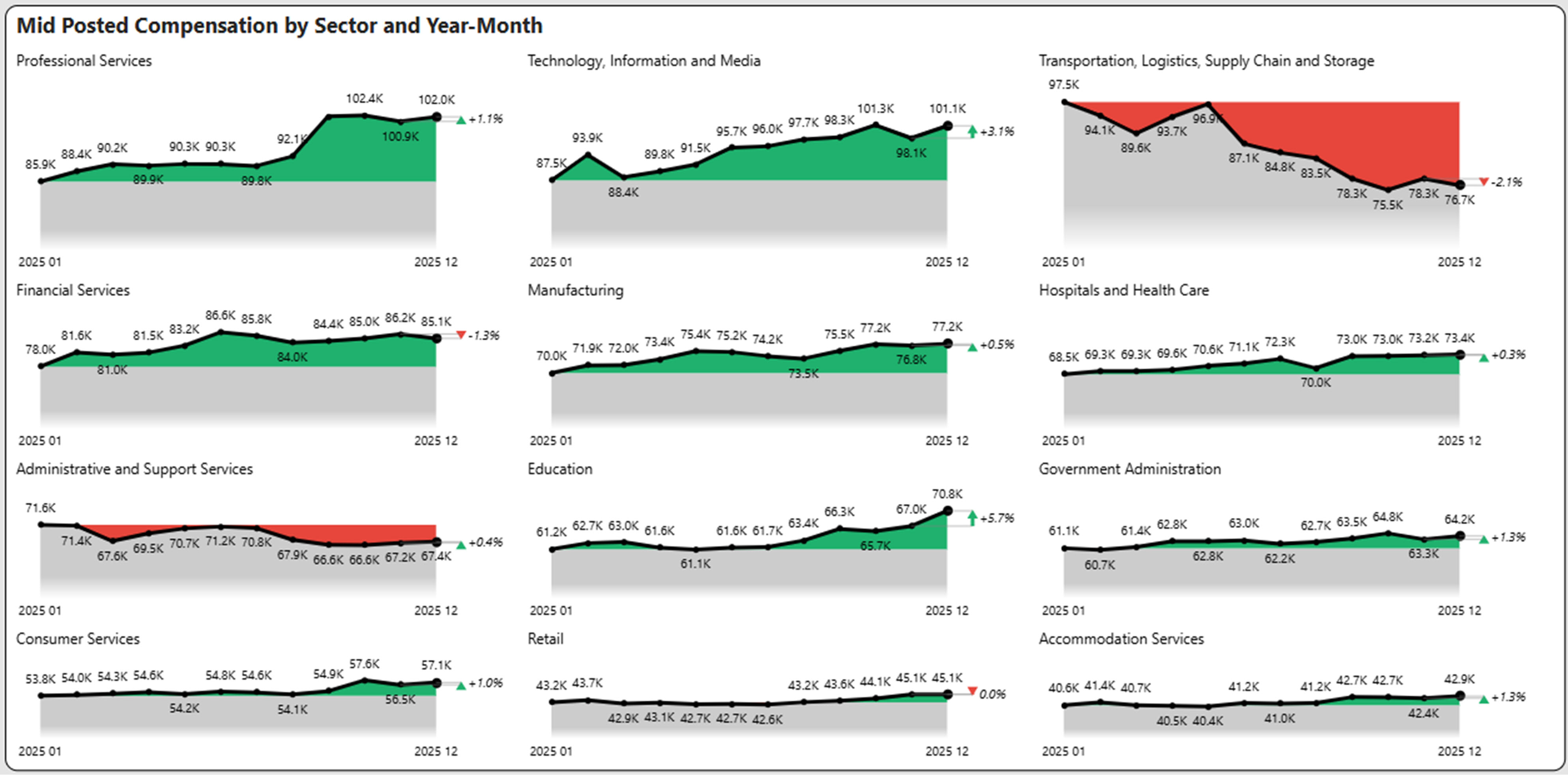

Industry Sector Compensation

The chart below shows the compensation by industry sector for the year, which clearly shows the winners and losers.

Supply and Demand

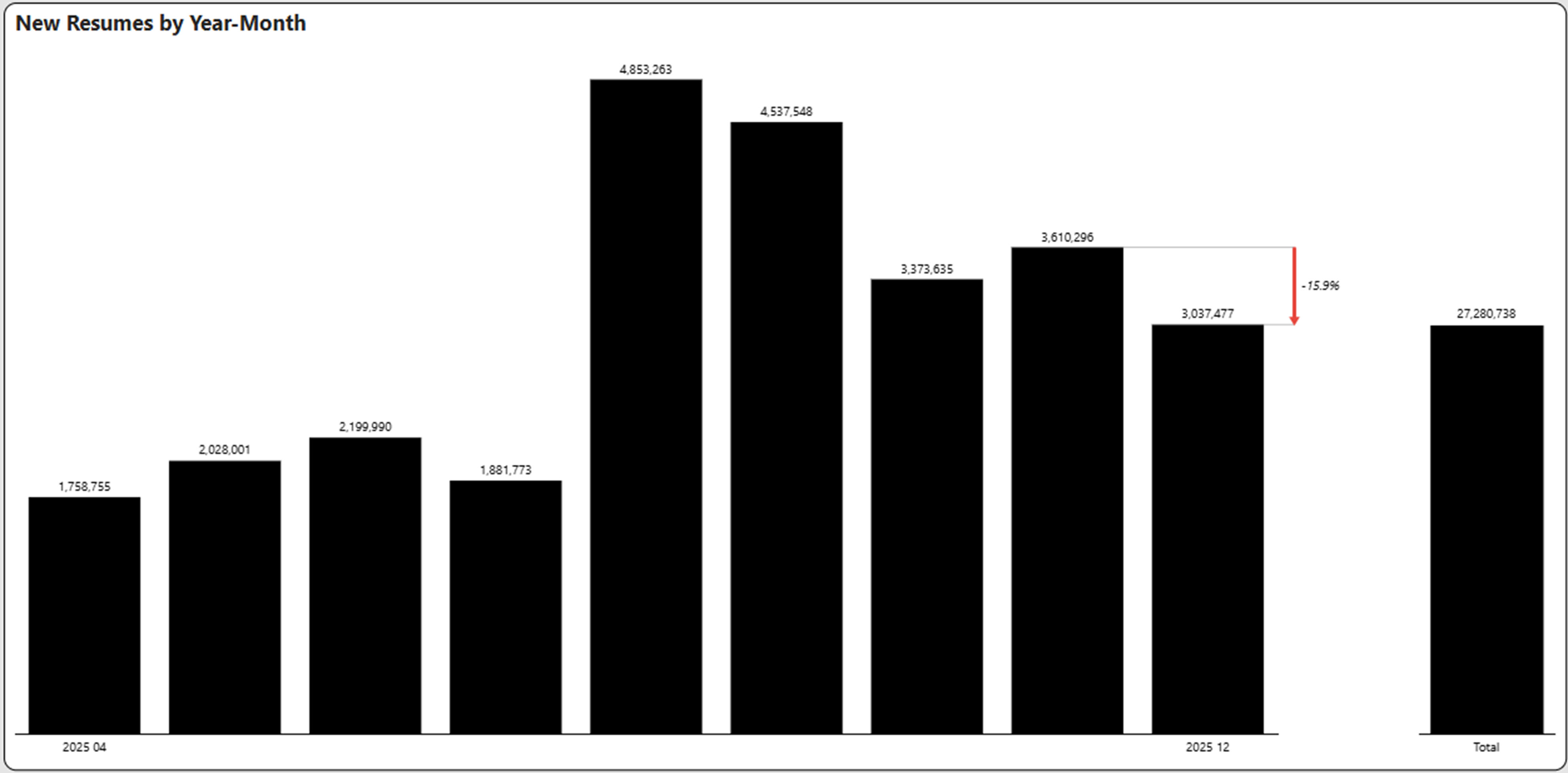

Trailing Resumes Continue Upward Climb

We review total resumes over the trailing nine months as an indicator to measure overall job seeker interest. Total trailing resumes over nine months increased 1.3% from 26.9 million to 27.3 million in December. December new resumes decreased by 15.9%, which could be contributed to a focus on the holidays instead of job seeking.

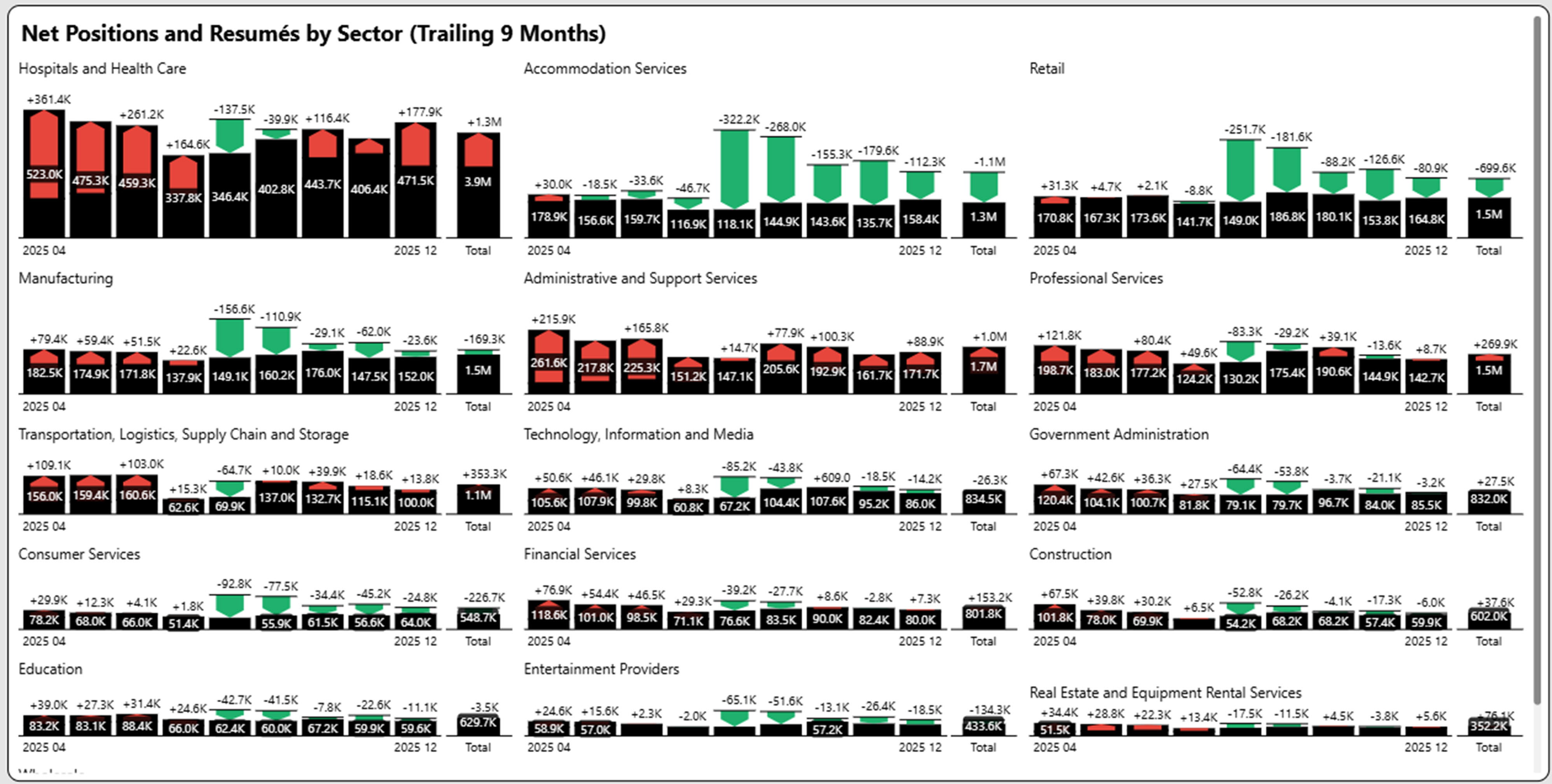

Supply/Demand by Industry Sector

To highlight supply/demand imbalances, we superimpose job seekers based on resumés against net job positions (hires based on unique postings) in black bar. The graphs highlight supply surplus (more job seekers than net postings) shown in green or supply shortage (less job seekers than net postings) shown in red. We picked a time period of nine months, which highlights the current market surplus or shortage. The total bar reflects the summaries of openings and resumés for that time period.

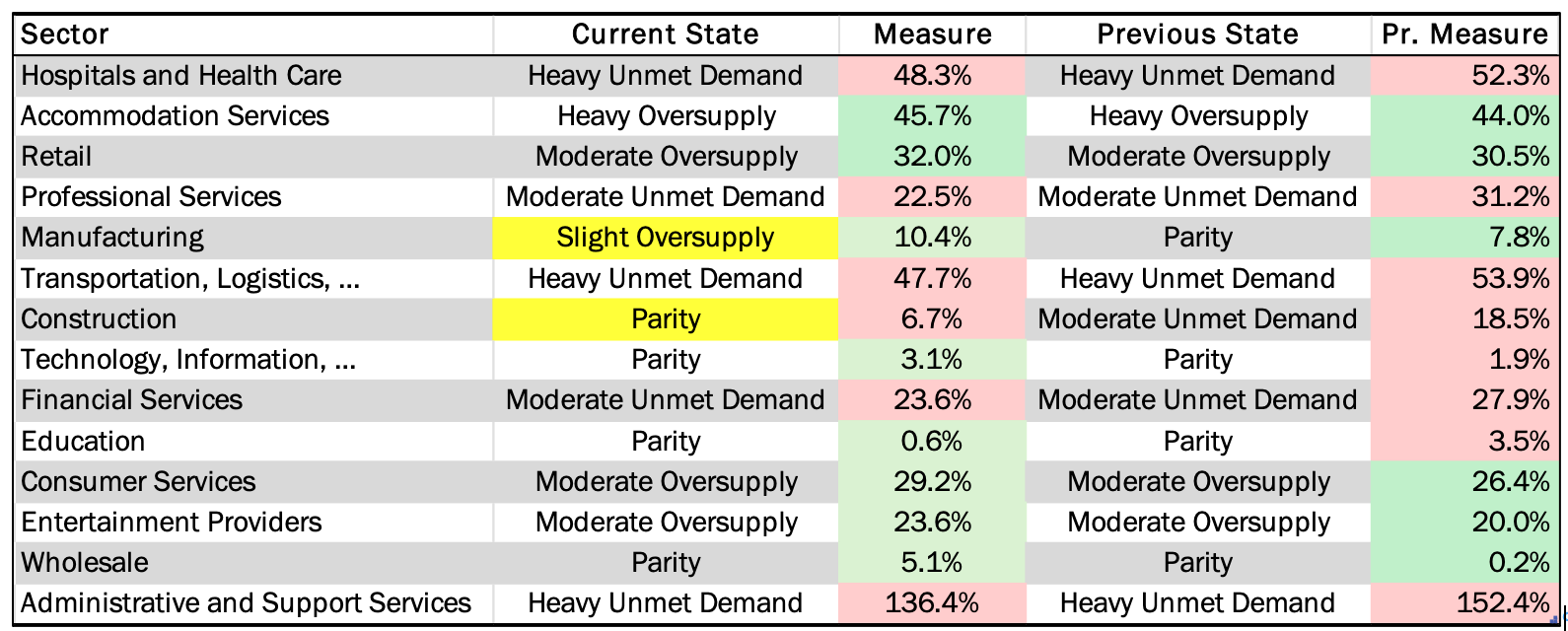

Supply/Demand Scorecard – Moving Towards Increased Supply

We highlight the current state at the end of December as well as the most recent changes over the last nine months. A change is not necessarily good or bad, but we have highlighted changes in supply/demand gaps that significantly impact the current trends.

In the graph below, the measure column shows the percentage of excess supply over demand (green) or demand over supply (red). The current monthly state is then compared to the previous monthly state with changes highlighted in yellow. Manufacturing and Construction both progressed towards higher supply over demand. All of the sector movement below is moving towards increasing supply availability.

Overall net positions for the trailing nine months decreased from 21.8 million to 20.4 million while resumes increased indicating further compression of the job market. Net positions are down 11% since September 2025.

Worker Sentiment

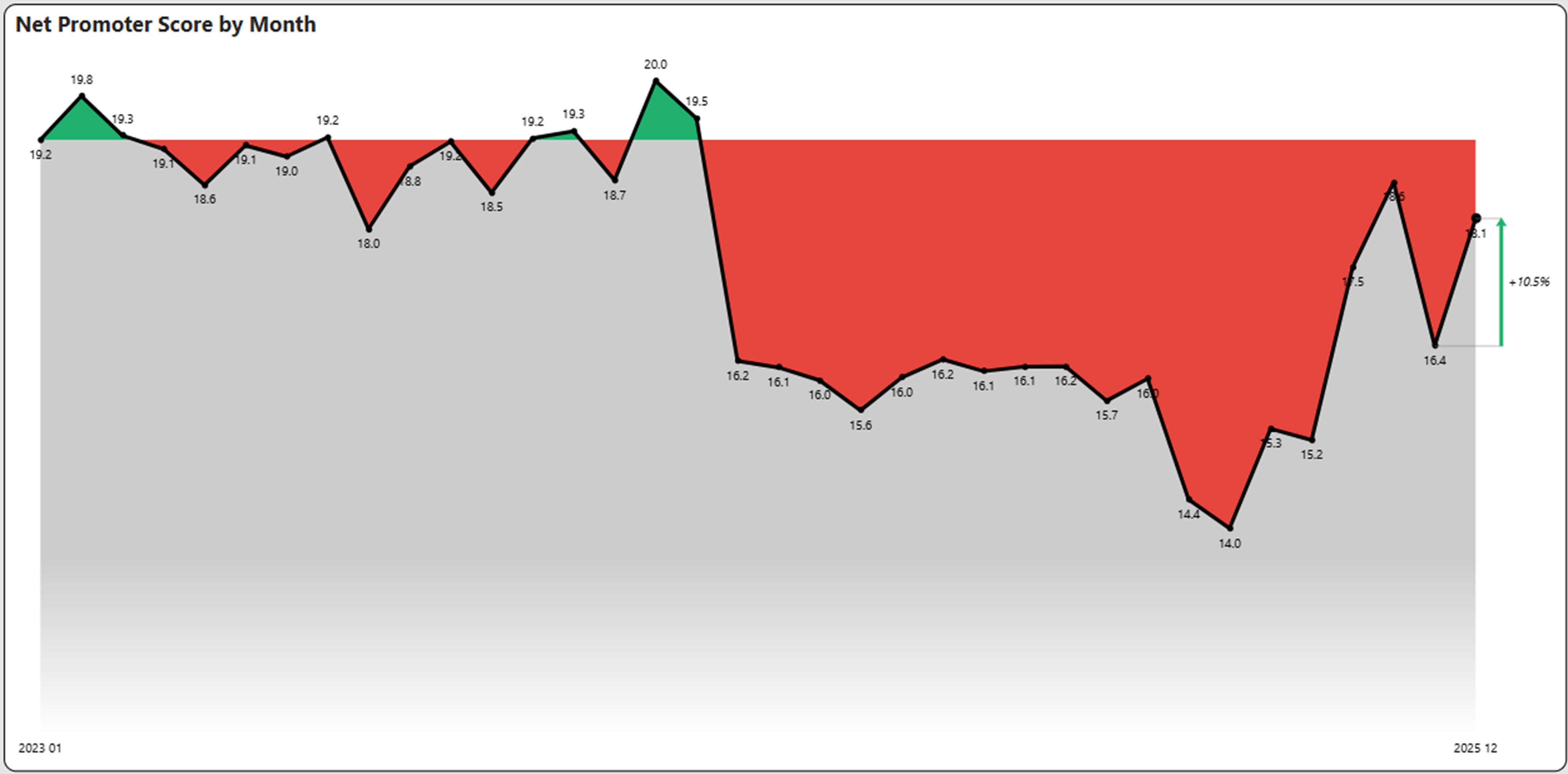

Net Promoter Score (NPS)

The Net Promoter Score (NPS) increased 10.5% in December after declining November. Net Promoter Score is defined as the percentage of positive reviews over negative reviews. NPS at 18.1 is 29.2% above the lowest point of 14, but still below the high point of 20.0.

Labor Market

Key Labor Market Takeaways

If You Liked the December 2025 Jobs Report – Get More Insights!

Try Our Free Version of TalentView to Get Instant Compensation, Postings, and Fill Days By Title, Company and Location (No Sign Up Required)

Example Insight: Employers with the most job postings Sept-Nov, 2025.

Current Competitive and Market Talent Intelligence is a Powerful Tool

What is TalentView?

Public Insight develops TalentView, a talent market intelligence solution that generated these insights. The most current and detailed insights are available by title, employer, location, industry and more. We provide flexible ways to utilize talent market intelligence, which include data licensing, interactive dashboards and reports.

How Can Our Must-Have Market Insights Help You?

- Justify Recruiting Decisions and Utilize Data to Tell Your Story

- Inform Recruitment Marketing Budgets, Strategies and Priorities

- Benchmark Employers Against Competitors

- Enhance Your Solution Offering (Solution Providers)

- Identify Business Development Opportunities (Solution Providers)

- Develop Content for Account Management and Marketing (Solution Providers)

Get Started!

Schedule a Call – Let’s discuss and demonstrate how you can leverage talent market data and insights

Sign Up for a Trial – Try out our interactive dashboards or get sample data